We’ve stressed for some time that the focus of our current strategy is to carefully manage the risk in client portfolios rather than reach for extra return. Given that positioning, it’s useful to explore some of the key considerations leading us to arrive at that strategy focus. We’ve written in the past about risks arising from the Fed’s aggressive posture, demographic problems in Japan, and European debt problems. Here, we’ll focus on the domestic front, although we expect to write an update on the European situation in the near future.

The domestic economy has been in a slow recovery mode for nearly three years. The job market is showing signs of progress, corporate earnings are reaching new highs, and the worst of the housing market decline is now likely in the rear view mirror. So it’s reasonable to ask whether we are now past the time when a risk management emphasis is warranted. Rather than weighing a wide and potentially conflicting array of economic and investment market data to address that question, a few focused insights on the economy and the stock market should shed light on our continued risk aversion.

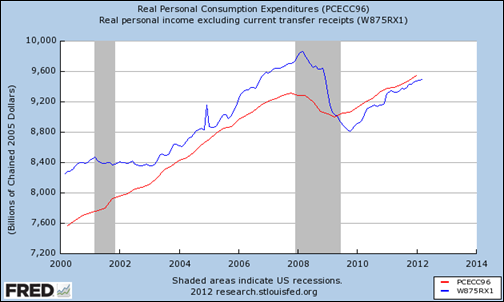

On the economic front, for many years consumer spending has been the driver of around 70% of U.S. economic output (GDP). So understanding the health of consumer spending should go a long way toward understanding the health of the economy. In the graph below, the red

line represents real (inflation-adjusted) consumer spending since 2000. One can see that in the 2001 recession, spending grew right through the recession while in the latest recession, spending fared much worse with a very sharp drop. Furthermore, although spending is now growing again and has surpassed the prior 2008 peak, the blue line on the graph, representing real personal income excluding government transfer payments (unemployment comp, Medicaid, Medicare, disability, etc.), suggests all is not well with the consumer. In the 2001 recession incomes flattened for a year after the recession, then quickly grew to new highs. Currently, well over two years into a recovery, real incomes excluding transfer payments are far lower than the pre-recession peak, while spending is higher. That’s not sustainable and shows the extraordinary extent to which the government is still supporting the economy. But for transfer payments, consumers would have to dip into savings just to support current spending. With the large and growing government debt problem, this highlights the dilemma the country faces: address the debt problems and potentially knock the props out from under the economy or ignore the growing debt and thereby add to the problem that will have to be faced in the future. So, while the economy is on the mend, we continue to think downside risks to the economy are elevated.

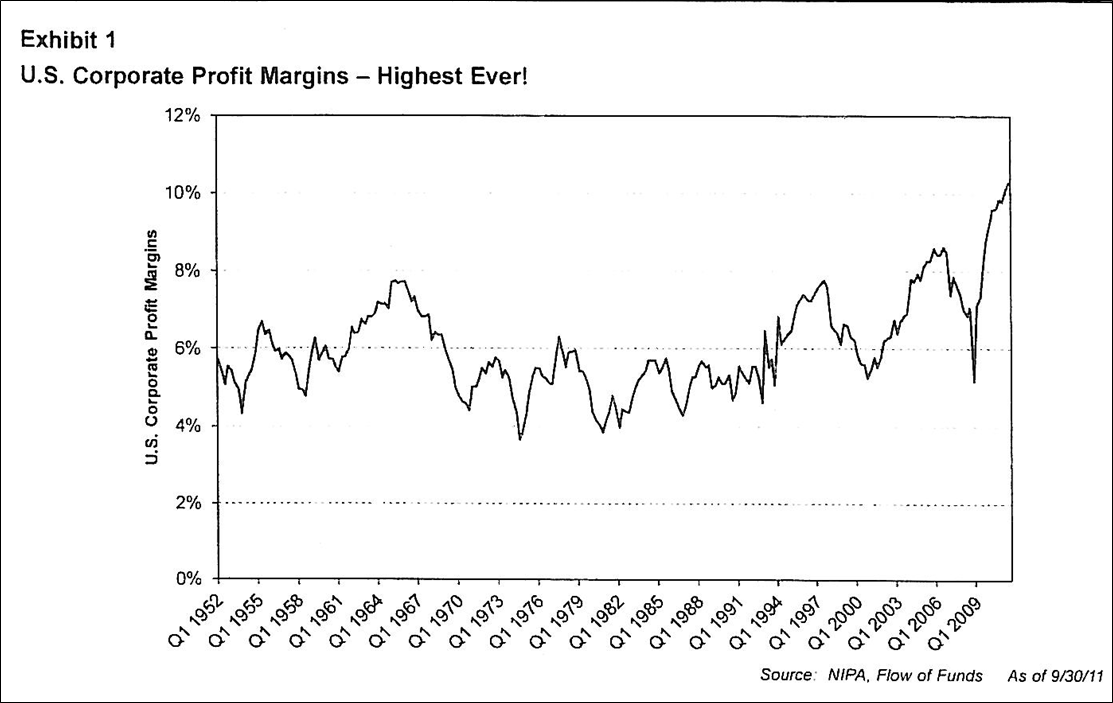

As for the stock market, we recognize that the market doesn’t look especially expensive on current earnings, particularly given the extremely low prevailing interest rates. However, the looming

question is the sustainability of these earnings levels. The graph below

tracks corporate profit margins (profits as a percentage of revenues) over the last 60 years. Profit margins have varied within a range of a couple of points above or below 6% over the entire period save for the last few years when they’ve vaulted above 10%, far higher than at any prior time. Both history and economic theory suggest that profits at some point will gravitate back toward the long-term norm of 6%. When this occurs, the market will no longer look reasonably priced. Put another way, the market is expensive compared to normalized earnings, but not on current earnings. We aren’t prepared to forecast the exact timing for when earnings normalize, but we do think the clock is ticking for the time when earnings come under pressure from shrinking profit margins.

Given the risks from an economy that continues to be highly dependent on government support and a stock market facing increasing risks of profit margin erosion, we think it makes sense to rein in portfolio risk by putting particular emphasis on quality and strong and growing dividends, while maintaining lower than normal exposure to riskier small-cap stocks.