"The test…is the ability to hold two opposed ideas in the mind at the same time."

-F. Scott Fitzgerald

After a mild dip in the first quarter, stocks resumed their advance in the second, and our blended stock index (70% broad US stocks and 30% broad international stocks) returned 11.8% in the first half of the year. Small and Mid-cap US stocks and emerging market stocks each did better than large US stocks, and the S&P 500 returned “only” 10.2% in the first half, its best in five years. Bond returns were slightly positive.

As the second quarter recedes, markets still face the same duality of long-term problems and opportunities. On the one hand, the federal debt is $39 trillion (on track for $40 trillion this fall), and the budget deficit is $1.9 trillion (6% of GDP) with $1 trillion in annual interest.

Compounding the debt problem, the stock market remains overvalued. The ratio of total US stock market value to GDP (“The Buffett Indicator”) has blown through historical extremes: the US stock market capitalization is now 219% of GDP versus a long-term average of 80-90%, and prior peaks of 115% in 2007, and 150% in 2000.

The Inflation Connection

As government debt increases, inflation will likely follow. Debt must be either paid or repudiated (a catastrophic option). Paying requires money from more government revenue (unlikely at current growth rates), lower government spending, more borrowing, or the creation of new money. Cutting spending is difficult as 86% of it is guaranteed benefits, interest on the debt, and defense spending. Borrowing and money creation are so much easier than other options politically that they are the most likely outcomes: mostly borrowing when the market will absorb it, creating money when it will not [technically, all the deficit is borrowed and then the Fed buys some of that with newly created money – for context, a bit over half of the cumulative deficit over the past 25 years has been “monetized”]. Compounding risks, most of the government bond issuance of late has been in short-term paper.

When the amount of money grows faster than the amount of goods and services in the overall economy, prices, the connection between the two, must adjust – that’s inflation. The most reasonable long-term outlook for inflation given unprecedented debt and intractable deficits is “higher for longer.”

The Other Possibility

On the other hand (and here comes the other part of the duality), there is one additional possibility: If the AI boom persists, broadens, and expands such that government tax revenues grow enough, we could grow out of this deficit and debt problem. The current phase of the AI boom is unlikely to prove an economic deliverer. The AI and data center buildout is real, and perhaps even in the early stages, but ultimately it is debt-driven and dependent on substantial productivity enhancements to follow - otherwise, the boom will eventually bust. However, if this massive AI investment (plus quantum computing plus the commercialization of vast potential in space) ultimately brings substantial and broad productivity gains, this has the possibility of boosting economic growth faster than government spending growth, and in that scenario, we could potentially grow our way out of our debt problem without having to inflate our way out.

Potential Portfolio Impact

We can’t handicap the likelihood of one path versus the other, but the two most likely long-term economic outcomes are either higher inflation or higher economic growth (and maybe a bit of both). In the long term, if we get higher inflation, that would generally be expected to be bad for bonds, and likely OK for stocks. And if we get materially higher long-term economic growth, that would generally be expected to be good for stocks even if not so great for bonds.

In either scenario, unsurprisingly, the long-term outlook for stocks would generally be expected to be better than that for bonds if we exclude the impact of current valuations. Stock valuations imply nothing about short-term returns, but high (expensive) stock valuations have historically been followed on average by sub-par returns. From here, both scenarios may imply modest future returns from bonds, perhaps not matching their coupons, while exceptionally high current stock market valuations may imply unexceptional long-term US stock returns looking forward. Together, lower than average long-term portfolio returns may be likely ahead in the long term. Mitigating that, better valuations for non-US stocks and for smaller US stocks alike portend better long-term opportunities for each than for large US stocks.

Warsh Factor

This is not new. What is new is the chairman of the Federal Reserve. Kevin Warsh has signaled a Fed more singularly focused on inflation, which could be a good thing in the long run, but carries a risk of higher short-term economic and market volatility. Moreover, each of his previous four Fed chiefs had to deal with a financial crisis of one sort or another within a couple years of assuming office. All that could accentuate financial bumps along the way in the near term, particularly with inflation running at 4.2% YoY per the latest CPI release (May), having remained above the Fed’s 2% target for five years.

IPO Irrationality

The other new thing is a suddenly awakened market for large initial public offerings (IPOs) with SpaceX appearing recently and at least Anthropic and OpenAI expected over the next several months. A brief look at the history of IPOs may be useful.

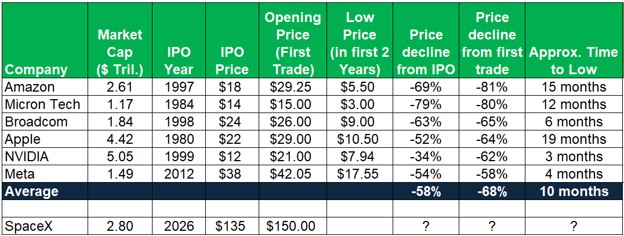

Most public companies that didn’t start as spin-offs went through an IPO at one point, and seven of the largest ten US companies did so within the last 30 years. Excluding Space Exploration Technologies (“Space-X”), they are, from most recent: Meta Platforms (“Facebook”), Tesla, Alphabet (“Google”). NVIDIA, Broadcom, and Amazon. It may be easy to think “I’d like some of that!”

The reality is that picking IPO winners is challenging, much like the challenge of picking any other stock winners – but with much less history and information. In fact, per a recent report from First Trust, of all US IPOs since 2006, 64.6% declined in their first year as a public company with a median decline of nearly 22%. Moreover, their median stock price declines each year in the next four years ranged between -22% and -33%. Yes, some have done quite well, but odds of selecting the strong performers are obviously slim. Less than half of the IPOs since 2007 were still around six years later.

Moreover, consider this selection from the largest US companies today, among the most successful IPOs ever. Had one selected them and been able to buy them on the IPO (often impossible), the buyer would still have had to ride out significant price drops within the first two years:

After their respective IPOs, the stocks of these great companies fell on average 58% from their IPO prices and 68% from their respective first trades within 3 to 19 months of their debut. In each case, much better entry prices after the IPOs became available for the patient.

Numerous short- and long-term uncertainties elevate risks, and mega-IPOs don’t appear to be the antidote. However, better valuations are available in non-US markets, in smaller stocks, and in some out-of-favor pockets of the market for larger stocks, and those opportunities seem now to be among the best in some time. That’s another way of saying that while IPOs may not be the opportunity some seem to believe, more broadly, the best “secret sauce” one can add to a portfolio remains a generous mix of discipline, patience, and diversification.

Uncertainty: No Argument Against Discipline

It’s tempting, after a strong market rebound, to conclude that previously identified risks were overstated. It’s equally tempting, when inflation persists and valuations stay high, to conclude markets are ignoring reality. We think both conclusions are too simple. Markets are not omniscient, but neither are they foolish. They weigh real risks against real strengths: inflation against earnings, high rates against productivity hopes, geopolitical uncertainty against resilient demand, and expensive US valuations against cheaper opportunities elsewhere.

We can’t predict the turns in that weighing process. We seek to build portfolios that can handle those turns. That means remaining invested, diversified, valuation-aware, and disciplined. It also means recognizing that the most important investment opportunities are not dramatic ones made in response to headlines, but quieter ones made in advance: to own quality, manage risks, keep enough liquidity, avoid excessive concentration, and to resist the emotional pull of recent performance.

The second quarter ends with markets in better shape than seemed likely only a few months ago. That’s welcome. But it’s not a reason to abandon caution, nor is caution a reason to abandon opportunity. A thoughtful portfolio should be able to hold both ideas at the same time.